401K/IRA Rollover

- Kiplinger: Myth Busters - Examining the Facts About Inded Annuities

- Employee Fiduciary: (Possibly) The Biggest Small Business 401(k) Fee Study Ever!

- Forbes: The Real Cost Of Owning A Mutual Fund

- Kiplinger: Myth Busters: Examining the Facts about Index Annuities

- Why Ken Fisher really LOVES Annuities! (And YOU should too!)

- Bloomberg: Fidelity to Baby Boomers: Lay Off the Stocks

- Forbes: Is A Fixed-Index Annuity Right For You?

- Yahoo Finance: The Downsides of 401(k)s That You’ve Never Heard Of

- Kiplinger: Benefits of Doing Roth IRA Conversions Early in Retirement

- ThinkAdvisor: Why Ken Fisher is Wrong on Annuities

- Wall Street Journal: The Champions of the 401(k) Lament the Revolution They Started

- Forbes: The 7 Dirty Little Secrets Of 401(k) Plans

- InvestmentNews: Ken Fisher, famous annuity hater, invested in annuity companies

- Forbes: When To Replace Bonds With Annuities

- Riding Out the Retirement Red Zone with Fixed Index Annuities

- Time: Lifetime Income Stream Key to Retirement Happiness

- When Should You Consider A Roth Conversion

- CNBC: New report finds almost 80% of active fund managers are falling behind the major indexes

- Forbes: Stop Gambling With Your Retirement

- Kiplinger: When It Comes to Your RMDs, Be Very, Very Afraid!

- Yahoo Finance: Prepare for stocks to plummet 30% and a recession to strike any day now, legendary market prophet says

- Morningstar: Ed Slott: Roth Conversions Especially Attractive Before 2026

Annuities

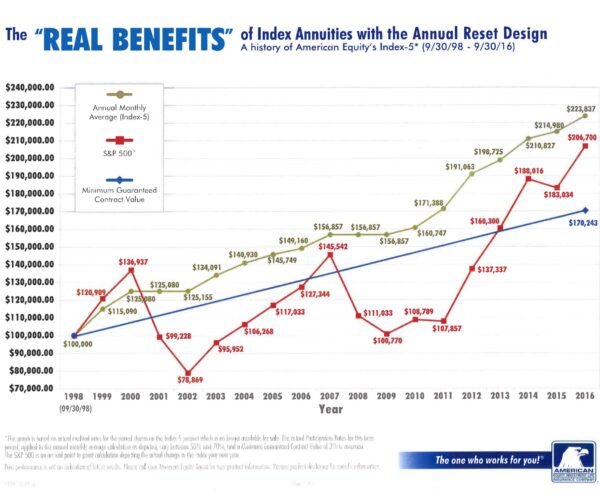

Annuities have become a very popular choice for 401k/IRA rollovers, and for those looking to secure guaranteed income that they cannot outlive. Annuities can help individuals save safely for retirement and earn interest linked to key stock market indexes, without the fear of stock market loss. In years where the market has gains, policyholders can get earn interest for the gains up to certain limits, or caps, but in years when the markets decline, policyholders will not experience any loss. This type of annuity is called a Fixed Index Annuity.

Click here for Annuities White Paper: Retirement By Design: Annuities Perception vs. Reality

Types of Annuities

There are two basic types of Annuities: Fixed and Variable.

Fixed Annuities have the interest rate is a stated, pre-determined rate for a period of 3, 5 or 7 years

Fixed Index Annuity where the interest credits are linked to the returns of key stock market indexes, but can never be negative.

Both Fixed Annuities and Fixed Index Annuities provide guarantees that the account will never drop in value due to stock market loss.

Variable Annuities are a product of the insurance and the securities industry. Funds are invested in the stock and bond markets via professionally managed subaccounts. As such, policyholder funds are directly invested in the markets and values will fluctuate with market gains and losses. The full fee structures are buried in the product prospectus. I do not recommend Variable Annuities as they have high annual fees (3-5% of the account balance) and are exposed to stock market losses.

Common Annuity Myths

Myth 1: My Money Is Locked Away and Can't Be Touched

With Fixed-Index annuities, you can withdraw money whenever you want. You can withdraw 10% of the account balance at any time without paying early withdrawal fees called surrender charges. Surrender charges decrease each year until the end of the surrender period, usually 7-10 years, at which time the surrender charges expire enabling you to access all of your funds without early withdrawal charges. Surrender charges are waived for death and certain health conditions such as confinement to a skilled nursing facility.

Myth 2: When I Die, the Insurance Company Keeps My Money

With the new Guaranteed Lifetime Income Riders (GLIR), clients no longer need to "annuitize" in order to receive income. The GLIR provides lifetime income that you cannot outlive even if you deplete the cash balance of the annuity. At death, any funds remaining in the annuity will be paid directly to your beneficiaries.

Myth 3: Annuities Are Expensive

Variable annuities can be very expensive with annual fees from 3-5%. However, Fixed-Index Annuities are usually ZERO fee products. With a Fixed-Index Annuity, all of your hard-earned savings will be working to generate growth guaranteed never to drop in value due to stock market losses.

Myth 4: Annuities Charge High Commissions

This may be true with Variable Annuities, but with Fixed-Indexed Annuities, agents are paid by the insurance company, not by you. 100% of your funds are working for you without one penny EVER being paid in agent commissions.

What is your COMRA Score?

The Color of Money Risk Analysis (COMRA) explores how you feel about potential gains and losses, examines the predictability of your assets, and provides a road map to your overall risk preferences. The output will be a Color of Money risk score. This short, interactive analysis is one of the first steps on the road to retirement. It's a short eleven questions that will take less that 5 minutes to complete.